We equate wealth with “net worth,” the sum total of your assets minus liabilities. Assets can include everything from an owned personal residence and cash in savings accounts to investments in stocks and bonds, real estate, and retirement accounts. Liabilities cover what a household owes: a car loan, credit card balance, student loan, mortgage, or any other bill yet to be paid. In the United States, wealth inequality runs even more pronounced than income inequality.

The Richest Americans

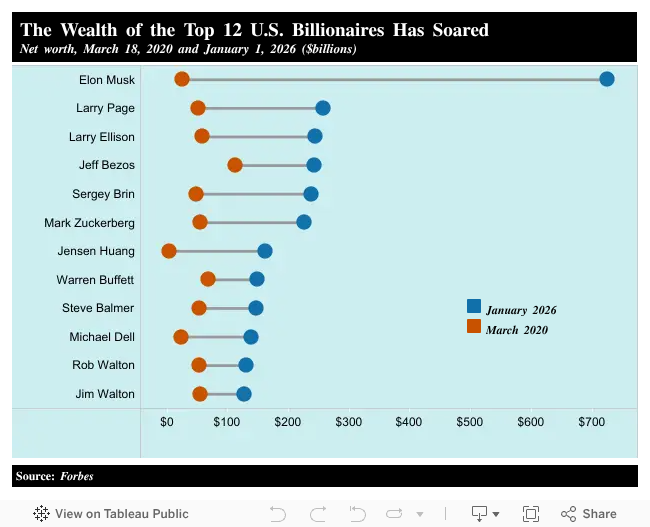

As of January 1, 2026, the collective net worth of America’s top 12 billionaires now surpasses $2.7 trillion. Their combined wealth has more than quadrupled, up from $608 billion on March 18, 2020, according to Institute for Policy Studies analysis of Forbes Real Time Billionaire Data.

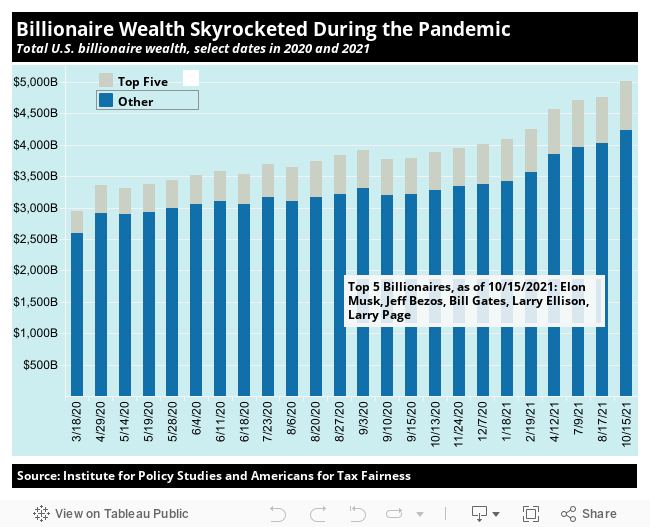

Even during the most intense period of the pandemic, as ordinary people around the world suffered from Covid-related health and economic crises, billionaires saw their fortunes expand. According to Institute for Policy Studies analysis of Forbes data, the combined wealth of all U.S. billionaires increased by $2.071 trillion (70.3 percent) between March 18, 2020 and October 15, 2021, from approximately $2.947 trillion to $5.019 trillion. Of the more than 700 U.S. billionaires, the richest five (Jeff Bezos, Bill Gates, Mark Zuckerberg, Larry Page, and Elon Musk) saw a 123 percent increase in their combined wealth during this period.

In 1982, the “poorest” American listed on the first annual Forbes magazine list of America’s richest 400 had a net worth of $250 million in 2025 dollars. The average member of that first list had a net worth of $750 million. In 2025, rich Americans needed a net worth of at least $3.8 billion to enter the Forbes 400, and the average member held a net worth of over $16 billion, over 21 times the 1982 average after adjusting for inflation.

Inequality is skyrocketing even within the Forbes 400 list of America’s richest. As of June 2026, Elon Musk, the richest member of this group, became the world’s first trillionaire. His net worth was 175 times larger than the net worth of the richest member in 1982 (in today’s dollars). Since 1982, just eight men have held this spot: shipping magnate Daniel Ludwig (1982), oil executive Gordon Getty (1983-1984), Walmart founder Sam Walton (1985-1988), media company owner John Kluge (1989-1991), Microsoft founder Bill Gates (1992-2017, except 1993), investor Warren Buffett (1993), Amazon founder Jeff Bezos (2018-2021), and Tesla and SpaceX CEO Elon Musk (2022-2026).

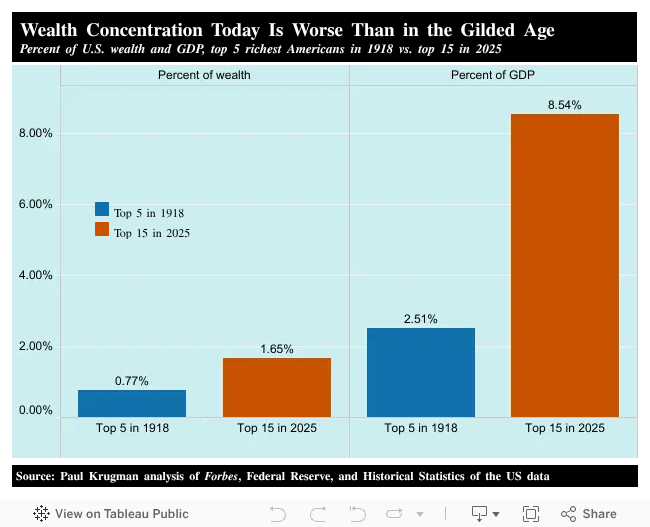

Comparing the wealthiest Americans in 1918 and 2025, economist Paul Krugman finds that today’s top fortunes represent a significantly larger share of both national wealth and economic output than they did during the Gilded Age, an era commonly associated with the extreme concentration of wealth. Adjusting for population growth, Krugman compares the five richest Americans in 1918 with the 15 richest Americans in 2025 (the U.S. population has more than tripled over this period). Today’s top 15 hold wealth equal to 1.65 percent of all U.S. wealth and 8.54 percent of GDP, compared with 0.77 percent of wealth and 2.51 percent of GDP for the top five in 1918.

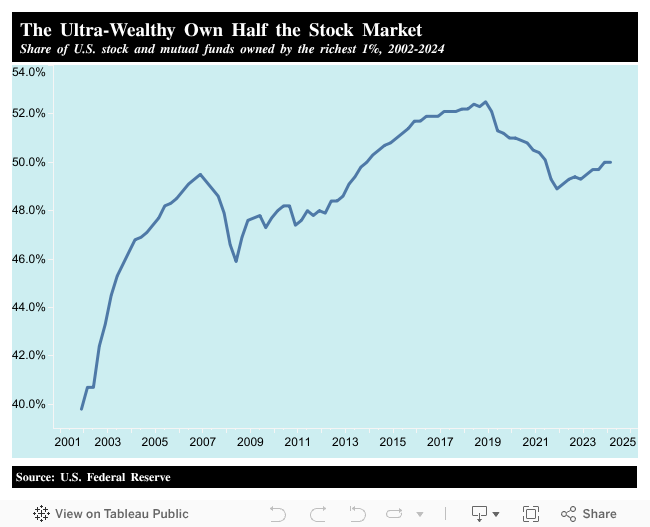

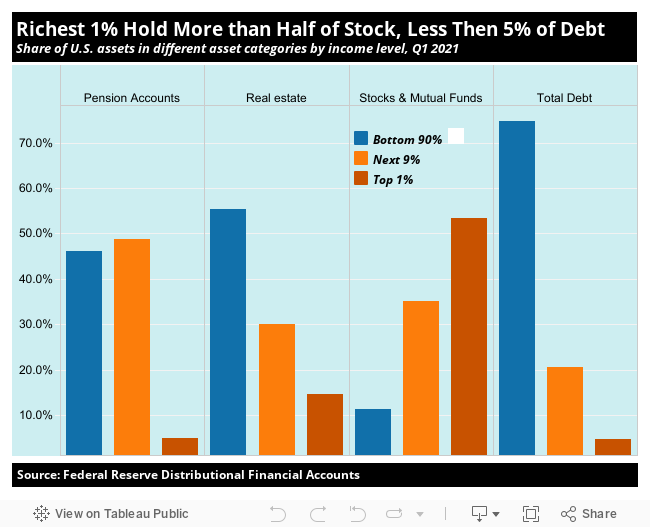

Another indicator of wealth concentration: the richest 1 percent own 50 percent of U.S. stock and mutual funds, up from 40 percent in 2002, according to Federal Reserve data.

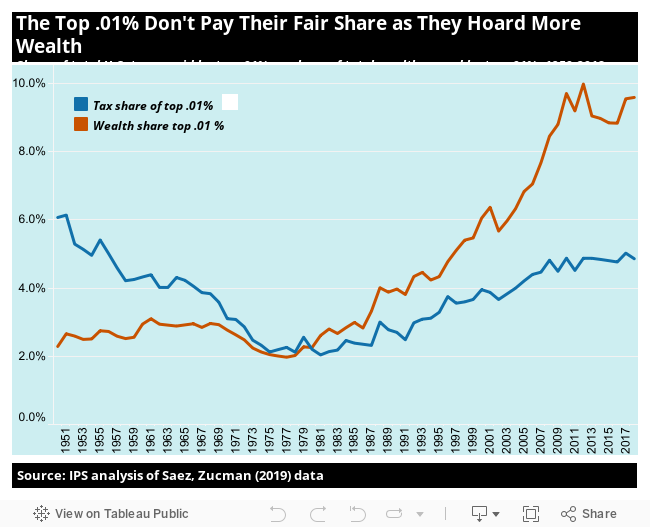

According to IPS analysis of Saez and Zucman data, as America’s richest .01 percent have accumulated more wealth, they have paid a smaller share of total U.S. taxes. In 2018, the tax share of the top .01 percent was close to what it was in 1953. By contrast, their share of the nation’s wealth nearly quadrupled during that period, rising from 2.5 percent to 9.6 percent.

America’s billionaires have increasingly used their exploding wealth to influence U.S. elections. According to Americans for Tax Fairness analysis, 100 billionaire families spent a staggering $2.6 billion, or 16.5 percent of total political contributions in 2024. In 2000, billionaire election spending came to just $18 million to influence the election, or 0.6 percent of total political contributions.

Household Wealth

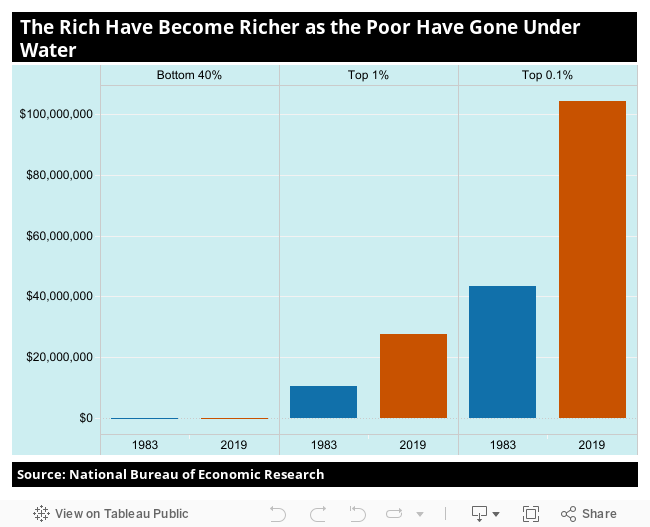

Over the past three decades, America’s most affluent families have added to their net worth, while those on the bottom have dipped into “negative wealth,” meaning the value of their debts exceeds the value of their assets, according to National Bureau of Economic Research data.

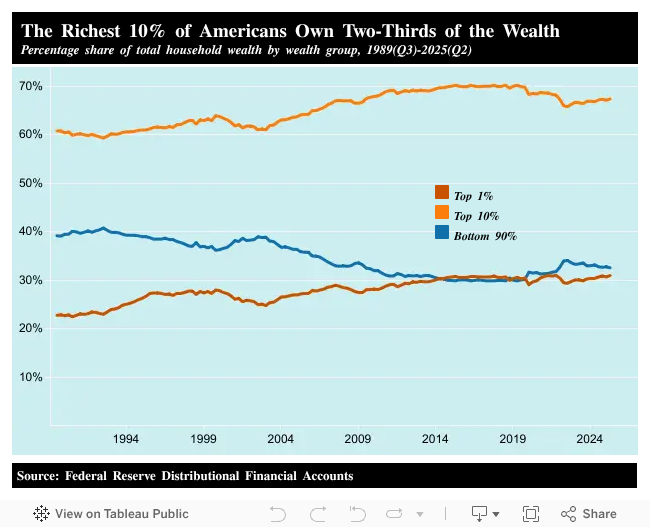

Since 1989, the share of America’s wealth held by the nation’s wealthiest has risen steadily. Federal Reserve data shows that the richest 10 percent of American households now own over two-thirds of the nation’s total wealth. The top 1 percent holds 31.0 percent of total wealth – just slightly less than the entire bottom 90 percent of U.S. households.

The rich don’t just have more wealth than everyone else. The bulk of their wealth comes from different — and more lucrative — asset sources, as the Federal Reserve’s Distributional Financial Accounts data shows. America’s top 1 percent, for instance, holds more than half the national wealth invested in stocks and mutual funds. Most of the wealth of Americans in the bottom 90 percent comes from their homes — the asset category that took the biggest hit during the Great Recession. These Americans also hold just around three-quarters of America’s debt.

The Racial Wealth Divide

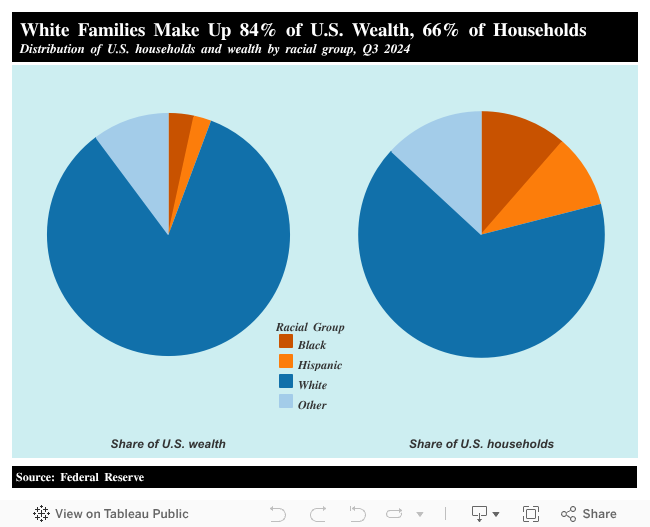

Public policies that favor white Americans and the wealthy have perpetuated both an extreme concentration of wealth and an extreme racial wealth divide. White households, Federal Reserve data show, held 84.2 percent of all U.S. wealth as of the fourth quarter of 2023, while making up only 66 percent of households. By contrast, Black families accounted for 11.4 percent of households and owned 3.4 percent of total family wealth, while Hispanic families represented 9.6 percent of households and owned 2.3 percent of total family wealth. These wealth figures include the value of consumer durable goods, such as vehicles.

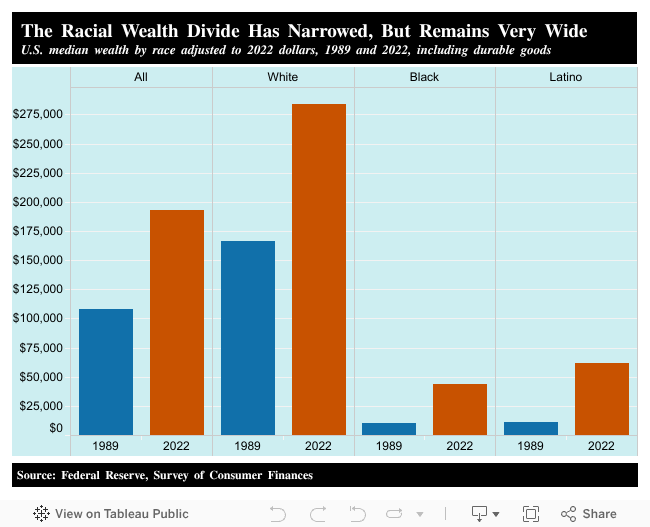

The racial wealth divide, according to Survey of Consumer Finances data, has narrowed slightly since 1989, but remains extremely wide. The median Black family has a net worth (including cars and other durable goods) of $44,100, just 15.5 percent of the $282,310 median white wealth. The typical Latino family, with $62,120, owns just 21.8 percent of the wealth of the median white family. The Institute for Policy Studies report, Ten Solutions to Bridge the Racial Wealth Divide, offers proposals for bold, structural reforms to address this problem.

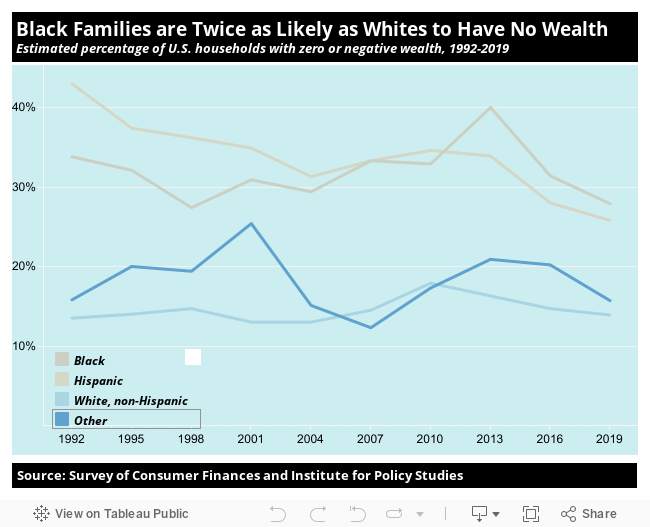

Families that have zero or even “negative” wealth (meaning the value of their debts exceeds the value of their assets) live on the edge, just one minor economic setback away from tragedy. Institute for Policy Studies analysis of Federal Reserve data shows that an estimated 28 percent of Black households and 26 percent of Latino households had zero or negative wealth in 2019, twice the level of whites.

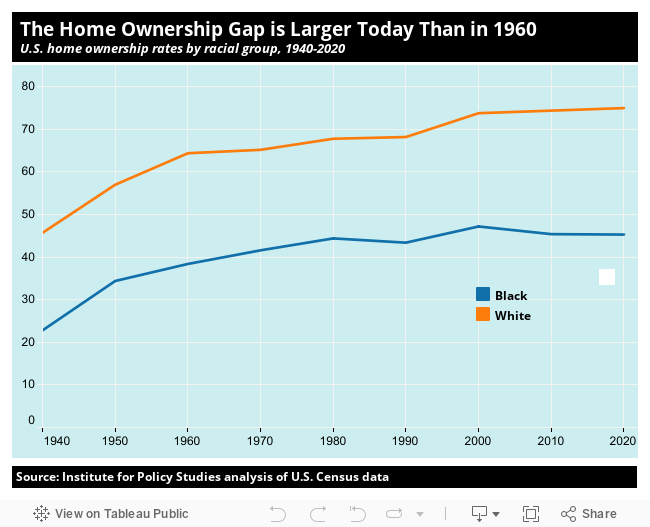

As with total wealth, home ownership is heavily skewed towards white families, our 2023 report with the National Community Reinvestment, Still a Dream, shows. Between 1960 and 2020, the rate of Black home ownership increased but the gap in ownership rates between Black and white families widened, from 26 percentage points to 30. Structural barriers, including lower incomes, higher rates of mortgage denials, and racial segregation, deny many Black families the opportunity to acquire this wealth-building asset.