Republican Tax and Spending Law Is Economically Misguided and Deeply Unfair

Cutting taxes for the wealthy and businesses and paying for it with Medicaid cuts will not have a positive impact on growth but will deepen the deficit and widen inequality.

Several provisions of the 2017 Tax Cuts and Jobs Act (TCJA) are set to expire at the end of this year, including its cut of the top marginal income tax rate from 39.6 percent to 37 percent. Discussions about whether to extend these provisions or allow them to lapse are intensifying in Congress.

Recent reports — such as this one and this one — suggest a potentially significant development: Some Republicans may be open to considering raising taxes on high-income individuals.

Whether this development will lead to actual substantive policy change is unclear. What is clear is that persistent government deficits and rising debt projections leave little room for more tax cuts.

Still, the fact that the conversation is even happening reflects a meaningful shift — and it’s a welcome one. In four of the last six major tax reforms (1986, 2001, 2003, and 2017), Republicans in Congress have cut taxes for high earners more than they have cut taxes for other groups.

If anti-tax policymakers have any lingering concerns about higher taxes on the rich hurting economic growth, here’s some news: They don’t.

Recent analysis by our team at the Institute for Macroeconomic and Policy Analysis (IMPA) at American University finds that allowing the TCJA’s top rate provision to expire would not negatively affect U.S. economic performance. The commonly assumed growth benefits of lower top rates are effectively neutralized by countervailing economic forces.

What does cutting the top rate do? It increases inequality in after-tax income and weakens the government’s fiscal position. The net impact on overall economic welfare is certainly negative.

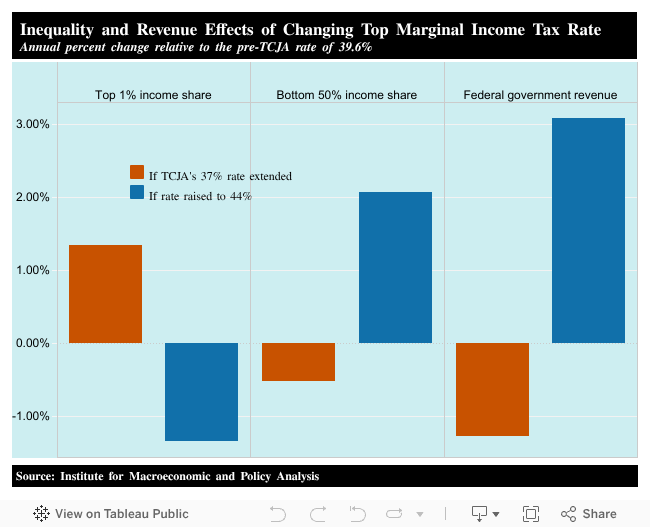

The figure below summarizes IMPA’s analysis. If the temporary provisions affecting the top marginal income tax rate are allowed to expire, the rate will revert to 39.6 percent, its pre-TCJA level. In this case, we estimate that the top 1 percent of taxpayers would receive 14.9 percent of after-tax national income.

If Congress makes the TCJA’s cut to the top tax rate permanent, the after-tax income share of the top 1 percent would go up by approximately 1.3 percent in the long run, and the share received by the bottom 50 percent would go down by about 0.5 percent.

Alternatively, if Congress were to modestly raise the top marginal rate to 44 percent — an illustrative rate that is aligned with recent discussions among some Republican lawmakers — the top 1 percent’s income share would decline by 1.34 percent, while the bottom 50 percent’s share would rise by 2.07 percent.

Of course, income tax cuts for the rich reduce government revenue in the short run. Our research shows that’s true in the long run, too. Keeping the TCJA’s cuts would reduce annual federal revenue by almost 1.3 percent in the long run compared to allowing expiration. In the 2023 budget, that would have been enough to pay for about half of the annual cost of the Supplemental Nutrition Assistance Program (SNAP).

In contrast, increasing the top marginal rate to 44 percent would raise annual federal revenue by approximately 3.1 percent in the long run. That would be about enough to pay for a year of SNAP, Children’s Health Insurance Program, and Temporary Assistance for Needy Families.

Our analysis also shows that the supposed trickle-down effects of tax cuts for high earners fail to materialize.

To understand why, it’s helpful to look at the sources of income of the top 1 percent of taxpayers. According to data from the Congressional Budget Office, wages account for just 32 percent of their taxable income, while 22 percent comes from ownership of “pass-through” businesses. These include law firms and other entities that are not subject to corporate taxes because their income “passes through” the business and is reported on owners’ individual tax returns.

This stands in sharp contrast to the bottom 80 percent of households, who derive most of their income from labor (66 percent) and Social Security (30 percent), while pass-through income makes up just 3 percent.

(The top 1 percent also gets 35 percent of its income from capital gains and dividends, while the bottom 80 percent gets just 1 percent of its income that way.)

Ignacio González is Co-Director of IMPA and Assistant Professor of Economics at American University.

Mary Hansen is Co-Director for Administration and Professor of Economics at American University.

Juan Montecino is Co-Director of IMPA and Assistant Professor of Economics at American University.

Aina Puig is research assistant at IMPA and a PhD candidate in Economics at American University.