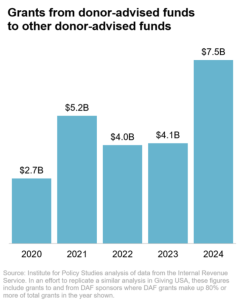

Since 2020, we have tracked the money cycling between donor-advised fund sponsors. We found $23.5 billion over the five years from 2020 to 2024, and $7.5 billion in 2024 alone — all of which counts, technically, as grants made to charity.

Why do DAF-to-DAF grants matter?

Donor-advised funds, or DAFs, are financial accounts managed by charities. When a charity manages a DAF, it is called a DAF sponsor. Donors can put money into DAFs and take a tax deduction immediately, because they’re technically giving to a charity (the sponsor). But the sponsor then gives the donors broad advisory privileges to recommend grants from the DAF — and the sponsor nearly always gives the grants to the recipients and on the timeline the donors want.

DAFs have been the fastest-growing segment of the charitable sector for more than a decade. Collectively, all DAF sponsors held $328 billion in assets at the end of 2024; at last count they took in 23 percent of all U.S. individual giving; and they now make up eight of the top 10 charities in the U.S, including the top five.

DAFs can be great for their donors. They provide significant charitable tax deductions, including for complex assets like stock and real estate, while at the same time giving donors a huge amount of control over when and where the grants go out.

Unfortunately, though, because DAFs have no payout requirement at all, the money in these funds often fails to move quickly to working charities directly addressing urgent needs. And because DAFs allow their donors to be completely anonymous to the public — even to the IRS and the organizations receiving their grants — there is no way for the public to make sure the money is moving. These DAF-to-DAF transfers add insult to injury, since they are reported to the IRS as grants. So when a big chunk of the money moves out of one donor-advised fund and into another, it inflates DAF grant numbers without actually sending funds to operating charities.

The numbers keep rising

We have been estimating DAF-to-DAF grants since 2018, when we first realized how significant the phenomenon was. To calculate our estimates, we draw from a similar analysis by Giving USA, the charitable sector’s gold standard report on giving trends, by looking at grants between sponsors where DAF grants made up 80 percent or more of total grants for both organizations.

What we found was that DAF sponsors gave more than $23.5 billion to other DAF sponsors over the four years from 2020 to 2023, and $7.5 billion in 2024 alone.

This DAF-to-DAF granting isn’t always necessarily going from one DAF account to another; for example, a DAF grant can go to a non-DAF account at a single-issue charity that also happens to be a DAF sponsor. Unfortunately, because we don’t have DAF grant information at this level of detail, we have no way of separating those grants out from other DAF giving.

This is one reason why we have restricted grant recipients in this analysis to those where DAF grants make up 80 percent or more of their total grants. And the vast majority — two-thirds — of this revolving grant money is both given and received by national DAF sponsors, where, for the most part, DAFs make up nearly all of their assets, revenue, and grants. When we looked only at grants going from national sponsors to other national sponsors, we found more than $18.2 billion going back and forth between national sponsors over the five years from 2020 to 2024, including $5.6 billion in 2024 alone.

In 2024, for example, DAFgiving360, formerly known as the Schwab Charitable Fund, gave more than half a billion dollars in grants to just three national sponsors: National Philanthropic Trust ($249 billion), Renaissance Charitable Foundation ($145 billion), and Fidelity Charitable ($128 billion).

No small potatoes

According to estimates from the DAF Research Collaborative, total grants from donor-advised funds were $64.6 billion in 2024. This means that the $7.5 billion given from DAF sponsors to other DAF sponsors represented nearly 12 percent of all DAF grants that year.

This is a sizable amount of money shuttling between donor-advised fund sponsors. And sponsors typically count this money towards their self-reported payout rates, even though it’s not actually getting to charities doing real work on the ground.

DAF-to-DAF granting can happen for several reasons that benefit or convenience the donor. Donors may switch between commercial DAFs when they change investment managers, because having their personal portfolio and their DAF held in the same institution makes management easier. They may want to take advantage of better giving advice, lower fees, or higher yields. Donors may switch between commercial DAFs because doing so makes it even harder to identify the actual donor, even for the sponsor. Or they may want to flee sponsors that are blocking their grant recommendations.

But we maintain that this sort of transfer shouldn’t count as charity. Donors get tax deductions for putting money into DAFs so that money can go to real charities — but, instead, it’s cycling between investment portfolios.

Our methodology

In our analysis, DAF grants are the grants reported on each grantor organization’s annual Form 990 return, Schedule D, Part I, Line 3(a). Following Giving USA’s methodology, we consider any transfer to be a DAF-to-DAF grant if grants from both the grantor and recipient make up 80 percent or more of total grants. We assign grants to the calendar year of the organization’s fiscal year end. For example, if a sponsor has a fiscal year ending in June 2023, we assign its grants to the 2023 calendar year.

For more, please see our previous reporting on this subject here.

Helen Flannery directs research for the Charity Reform Initiative of the Institute for Policy Studies.