Once they give it away, do donors still have control?

Helen: Yes. Legally, they have given up ownership of the money. They can’t get it back for their personal use. But, for all intents and purposes, they maintain control over the distribution of the funds and the ability to choose which charitable organization it goes to. It’s a bit of a fiction that these funds are “donor-advised” when they are really “donor-controlled.”

Why does this matter at all?

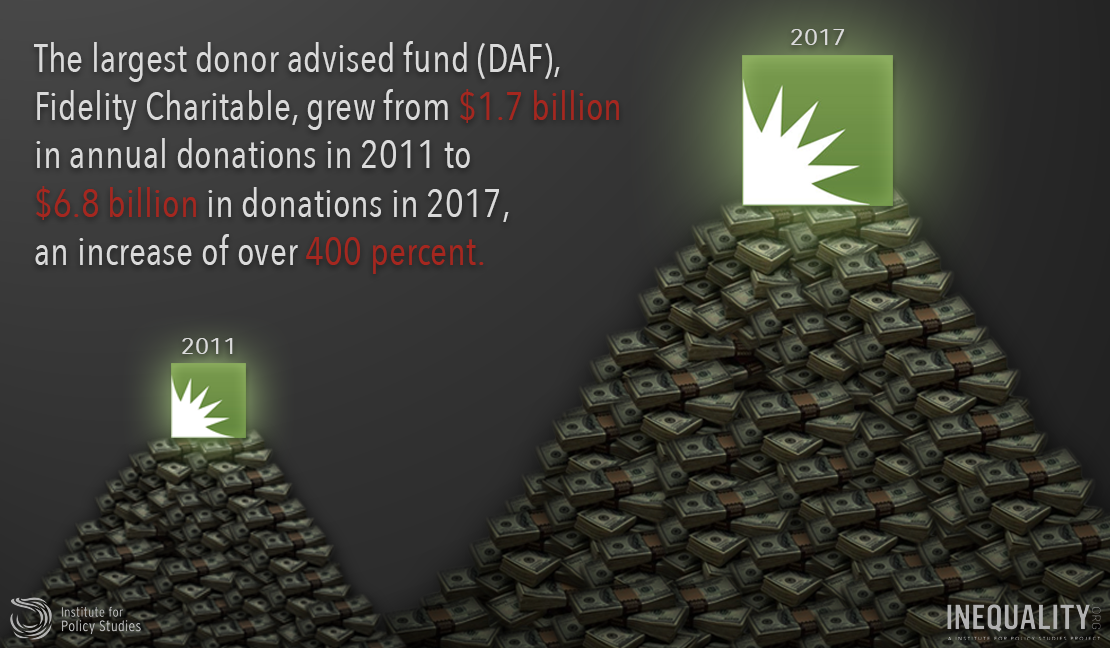

Helen: The problem is in the tax deductibility of donations to DAFs. Very wealthy individuals give money to DAFs and get a big tax break immediately for their gift. But then the money may sit for years, and sometimes forever, before it is distributed to active charities on the ground. The incentive system is broken. There is no incentive to move money out once it’s in the DAF. And, at least in the case of Wall Street sponsored DAFs, there are often incentives to keep money in the DAF.

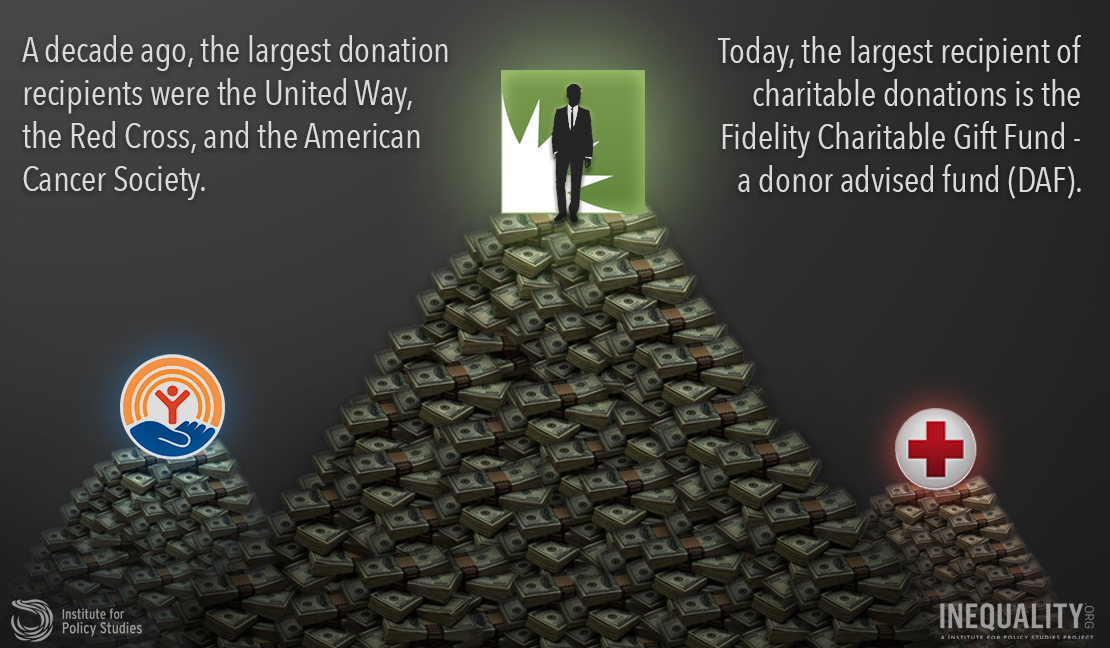

Nonprofit organizations should be very concerned that a bigger and bigger share of the charitable pie each year is going to DAFs, getting tied up indefinitely, and that a smaller and smaller share is going to organizations trying to solve problems for the social good.

Okay, so wealthy people are using the DAF system, but isn’t it their money to do what they want? And aren’t they giving it away to charities?

Chuck: I suppose it is positive that wealthy people are giving money to charity, even if the impact is delayed. It is better than hoarding wealth to buy another private jet.

If donors were not claiming a tax deduction, then it might be “their money to do whatever they want.” But because these donors are asking the rest of us to subsidize their donations through the tax code, there is a justifiable public interest to be monitored.

How do we subsidize the donations of billionaires?

Chuck: Through the US tax code, we provide major incentives for people to give to charity. We effectively say, “you can pay less taxes if you give to a qualified charity.” For every dollar a billionaire gives to charity, we the people subsidize 37 to 57 cents of that donation through diminished tax revenue.

So a billionaire is paying less for veterans’ services, public infrastructure, etc., in order to provide donations to charities entirely chosen by them. This is why there is a public interest in what they do with these funds. And this is why it’s a problem that people are claiming the tax break and then sequestering the funds for years before transferring to a real working charity.

Isn’t what you’re saying true for private foundations? Why pick on DAFs?

Helen: Yes, some of this is true. But private foundations have a legally mandated minimum payout. Every year, private foundations have to pay out five percent of their asset value. They also pay an annual excise tax. DAFs are required to do neither. There is no minimum DAF payout required at all.

Private foundations also have higher requirements for reporting and transparency, which protect the public interest and justify the taxpayer subsidy.

There is also a much higher risk of abuse with DAFs when donors are giving appreciated non-cash assets like artwork or real estate. The rules for valuing those types of assets for DAF donations are much more lax than they are for private foundations.